A chargeback is a forced reversal of a payment transaction, initiated by a cardholder through their issuing bank. Unlike a standard refund — which a merchant processes voluntarily — a chargeback bypasses the merchant entirely, returning funds directly to the customer’s account while the bank investigates the disputed transaction.

If you have ever seen a mysterious charge reverse on your credit card statement, or if you run a business that suddenly received a dispute notice from your payment processor, you have already encountered the chargeback system at work. Get List of top 10 Ecommerce Merchant Account Providers

This guide covers everything — the definition, step-by-step process, common reasons, a real-world example, the difference from a refund, and what merchants can do to protect themselves.

Key Takeaways: What You’ll Learn From This Guide

1. A chargeback is a bank-enforced payment reversal — not the same as a merchant-issued refund

2. The process involves the cardholder, issuing bank, card network, acquiring bank, and merchant

3. Common reasons include fraud, non-delivery, and billing errors — but friendly fraud is a growing risk

4. Merchants have a limited window to dispute chargebacks; missing it results in automatic loss

5. A chargeback ratio above 1% can put a merchant account at serious risk

6. Prevention is far less costly than resolution — invest in fraud tools, clear communication, and transparent policies

7. Consumers should always try to resolve issues with the merchant first before filing a chargeback

1. Chargeback Meaning — Defined Simply

The word “chargeback” is exactly what it sounds like: charging a payment back. When a cardholder disputes a transaction, their issuing bank can forcibly reverse the charge and pull the money back from the merchant’s account. Read About – Machine Learning Payments

The process exists because electronic payments were designed to be consumer-friendly. Card networks like Visa, Mastercard, and RuPay include chargeback rights as a foundational protection — a kind of safety net that makes people comfortable transacting online and in-store.Simple chargeback definition: A chargeback is a bank-enforced reversal of a completed payment, filed by a cardholder, that temporarily or permanently removes funds from a merchant’s account while the dispute is reviewed.

Chargeback vs. Dispute vs. Claim — Are They the Same?

These terms are often used interchangeably, but there are subtle differences:

- Dispute: The customer’s initial complaint, which may be raised with the merchant or the bank directly.

- Chargeback: A formal bank-initiated reversal following an unresolved or escalated dispute.

- Claim: Commonly used for buyer protection schemes (e.g., PayPal), which operate outside the traditional card-network chargeback process.

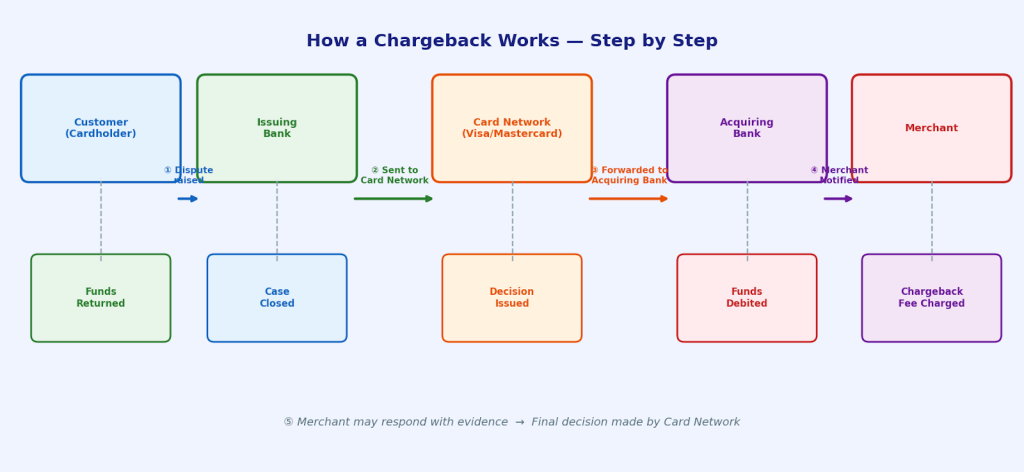

2. How Does a Chargeback Work? Step-by-Step

Understanding the chargeback lifecycle helps both consumers and merchants navigate it effectively. Here is how the process typically unfolds:

Step 1 — Customer Disputes the Charge The cardholder contacts their issuing bank (or uses the bank’s app) and formally disputes a transaction. Common reasons include fraud, non-delivery, or a billing error.

Step 2 — Bank Reviews the Claim The bank examines the dispute. In most cases, they provisionally credit the customer’s account while the investigation continues — meaning the customer has their money back before the case is even resolved.

Step 3 — Chargeback Initiated If the bank deems the dispute valid on the surface, it raises a formal chargeback against the merchant’s acquiring bank. Read About – Account Adult Merchant Online

Step 4 — Merchant Notified The acquiring bank (the merchant’s payment processor) notifies the merchant. Funds may be debited from the merchant’s account immediately, along with a chargeback fee.

Step 5 — Merchant Responds (Representment) The merchant has a limited window — typically 7 to 30 days depending on the card network — to submit evidence that the transaction was legitimate.

Step 6 — Second Review The issuing bank reviews the merchant’s evidence. If the merchant’s case is strong, the provisional credit to the customer is reversed and funds return to the merchant.

Step 7 — Arbitration (if required) If neither party accepts the second ruling, the dispute escalates to the card network itself (Visa or Mastercard) for final binding arbitration. This is expensive for both sides.

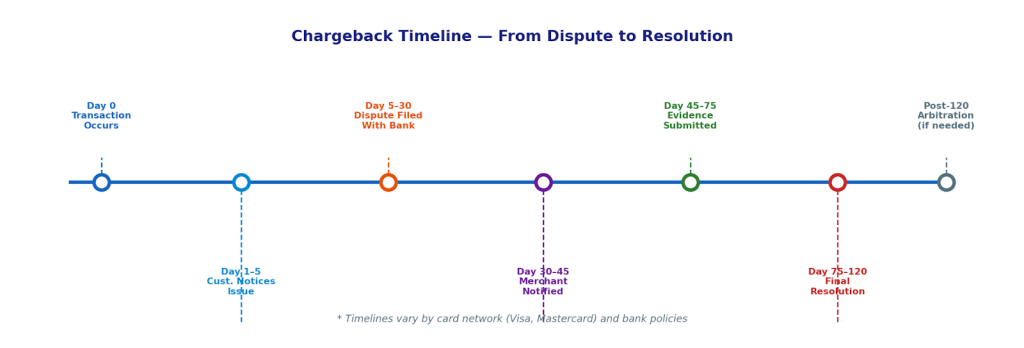

Key Timeframes to Know

- Customer filing window: Typically 60–120 days from transaction date

- Merchant response window: Usually 7–30 days from chargeback notification

- Full resolution: Can take 45 to 120+ days

- Arbitration (if escalated): Adds weeks or months to the timeline

3. Chargeback Timeline at a Glance

| Stage | Typical Timeframe | What Happens |

| Dispute filed | Day 0 | Customer contacts their bank |

| Bank review | Days 1–5 | Provisional credit issued to customer |

| Merchant notified | Days 5–45 | Funds debited, merchant alerted |

| Evidence submitted | Days 15–60 | Merchant sends representment docs |

| Arbitration (optional) | Days 30–90 | Card network steps in if unresolved |

| Final resolution | Days 60–120 | Funds awarded to winning party |

Note: Visa and Mastercard have slightly different chargeback windows. Always refer to your card network’s official dispute guidelines.

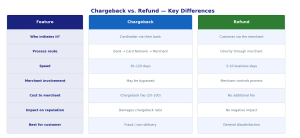

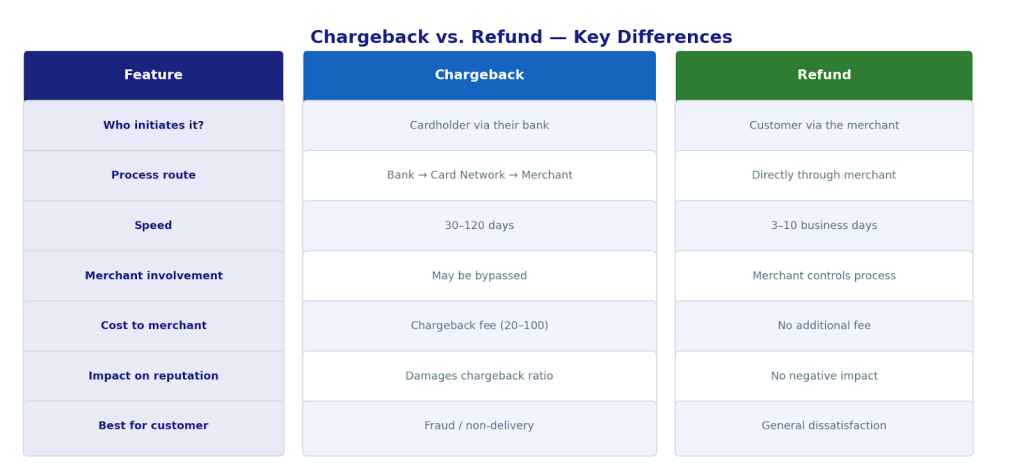

4. Chargeback vs. Refund — What Is the Difference?

This is one of the most commonly misunderstood distinctions in payment processing. Both result in the customer getting their money back — but the mechanism and consequences are fundamentally different.

| Factor | Chargeback | Refund |

| Initiated by | Cardholder via their bank | Cardholder directly with merchant |

| Process time | 45–120 days | Typically 3–10 days |

| Merchant fee | Yes — ₹500 to ₹5,000+ per case | No extra fee |

| Control | Bank makes final decision | Merchant decides outcome |

| Relationship | Adversarial | Collaborative |

| Fraud risk | High (friendly fraud possible) | Low |

| Credit impact | Can affect merchant’s account standing | No impact on merchant |

Why Does the Difference Matter?

For consumers, chargebacks are a powerful backstop — especially when a merchant refuses to issue a refund or is unresponsive. However, they are not meant to replace normal refund channels.

For merchants, a chargeback is significantly more damaging than a refund:

- A refund costs the merchant the product or service value only.

- A chargeback costs the product/service value plus a dispute fee.

- Too many chargebacks can raise the merchant’s chargeback ratio, leading to account termination or being placed on payment industry watchlists. Read About – Merchant Management System

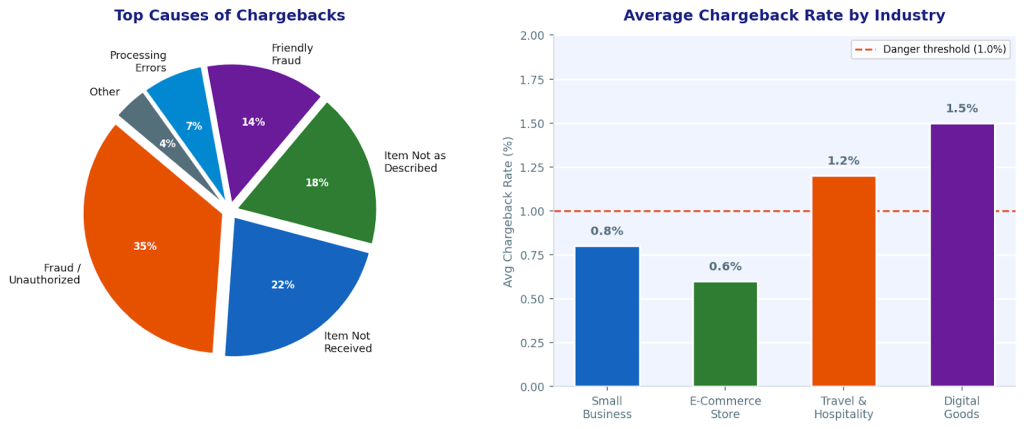

Industry Threshold: Both Visa and Mastercard consider a chargeback ratio above 1% (chargebacks ÷ total transactions) as a warning threshold. Merchants exceeding 2% may be classified as high-risk and face account termination.

5. Top 6 Reasons Customers File Chargebacks

1. Unauthorised Transaction (True Fraud)

The cardholder’s payment credentials — card number, CVV, or login details — were stolen and used without their knowledge. This is the most common and most legitimate chargeback reason. Card networks assign specific reason codes to these disputes (Visa: 10.4 / Mastercard: 4853).

2. Item Not Received (INR)

The customer paid for a product or service that was never delivered. This is common in e-commerce when shipments are delayed, lost, or when no tracking information was provided.

3. Item Significantly Not as Described (SNAD)

The product received was materially different from what was advertised. This includes counterfeit goods, damaged items, or products that did not match the listing description.

4. Billing or Processing Error

The customer was charged the wrong amount, charged multiple times, or an error occurred during the transaction. These cases are often resolved quickly once the merchant provides correct billing records.

5. Merchant Processing Error

A technical issue on the merchant’s side resulted in a failed or incorrect transaction, leaving the customer with an unexpected charge on their statement. Read About – Best PCI-Compliant Payment Gateways for Startups

6. Friendly Fraud (First-Party Fraud)

Friendly fraud — also called chargeback fraud — occurs when a customer files a chargeback for a transaction they knowingly authorised. Common scenarios include:

- Purchasing a digital product, downloading it, then claiming it was never received

- Buying a physical item, keeping it, and then disputing the charge

- A family member making a purchase that the primary cardholder does not recognise on the statement

Friendly fraud accounts for a significant and growing proportion of all disputed transactions globally — particularly in digital goods, subscription services, and travel.

6. Who Can File a Chargeback?

The right to file a chargeback belongs to the cardholder — the individual whose name is on the payment card. This includes: Get – Adult Credit Card Processing

- Credit card holders (Visa, Mastercard, American Express, RuPay, Diners Club, etc.)

- Debit card holders linked to a bank account

- Prepaid card holders, in some cases

Merchants cannot file chargebacks. They can, however, dispute a chargeback through the representment process (Step 5 above). Third parties — such as a family member using a shared account — may also be subject to chargeback rights, though the primary account holder bears legal responsibility.

7. Real-World Chargeback Example

The Scenario: Priya orders a ₹4,500 smartwatch from an online retailer. After three weeks, the product has not arrived. She contacts the merchant’s customer service twice but receives no response.

What Priya does: She calls her bank and files a chargeback under “Item Not Received.” Her bank provisionally credits ₹4,500 to her account within two days.

What happens next: The merchant is notified and has 14 days to provide delivery proof — tracking number, courier logs, or proof of dispatch. Since the item was never dispatched, the merchant has no evidence to submit.

The outcome: The chargeback is resolved in Priya’s favour. The merchant loses the ₹4,500 plus a dispute fee.

This example illustrates a legitimate use of the chargeback process. Now consider the reverse — the same scenario, but the watch was actually delivered and Priya simply decided she did not like it. Filing a chargeback instead of requesting a return would constitute friendly fraud. Get – Adult Site Merchant Account

8. How to Prevent Chargebacks — A Merchant’s Guide

Chargebacks are never entirely avoidable, but businesses that follow best practices can dramatically reduce their rate.

For Fraud Prevention

- Use 3D Secure (3DS2) authentication for all online transactions

- Implement real-time fraud scoring and velocity checks

- Require CVV and billing address verification (AVS)

- Flag multiple transactions from the same IP or device in a short period

For Dispute Prevention

- Use a clear, recognisable billing descriptor — customers should instantly know what the charge is

- Send order confirmation emails and shipment tracking notifications for every order

- Maintain a transparent refund and return policy, and make it easy to find

- Respond to customer service queries within 24 hours

- For subscription businesses, send reminder emails before each billing cycle

When a Chargeback Arrives

- Never ignore a chargeback notice — missing the response window is an automatic loss

- Gather all evidence: transaction records, signed contracts, delivery confirmation, communication logs

- Submit clear, organised documentation in your representment package

- Consider engaging a chargeback management specialist for high-value or complex disputes

9. Chargeback Reason Codes — Quick Reference

Card networks use standardised reason codes to categorise every chargeback. Understanding these codes is critical for merchants preparing a representation response. Get – Adult Payment Gateways

| Category | Visa Code | Mastercard Code | Common Cause |

| Fraud — Unauthorised | 10.4 | 4853 / 4863 | Stolen card or credentials |

| Item Not Received | 13.1 | 4855 | Product not delivered |

| Not as Described | 13.3 | 4853 | Product differs from listing |

| Duplicate Processing | 12.6 | 4834 | Customer charged twice |

| Credit Not Processed | 13.6 | 4860 | Refund not issued by merchant |

| Subscription Cancelled | 13.5 | 4841 | Charged after cancellation |

| Processing Error | 12.1 | 4831 | Incorrect amount charged |

Always refer to the official Visa and Mastercard dispute guidelines for the current and complete reason code listings.

Frequently Asked Questions

Q1. What is the difference between a chargeback and a refund?

A refund is a voluntary return of funds initiated by the merchant. A chargeback is a forced reversal initiated by the customer’s bank, bypassing the merchant entirely. Chargebacks carry fees and can affect a merchant’s standing with their payment processor.

Q2. How long does a chargeback take to resolve?

The typical chargeback cycle takes 45 to 120 days from the filing date to final resolution. Cases involving arbitration can take longer. The card network’s rules, the type of dispute, and how quickly both parties respond all influence the timeline.

Q3. Can a merchant win a chargeback dispute?

Yes. Merchants can win chargebacks by submitting compelling evidence during the representment stage — such as delivery confirmation, signed contracts, communication records, and transaction logs. The stronger and more organised the evidence, the better the outcome. Read About – Adult Merchant Account Instant Approval

Q4. Can I file a chargeback on a debit card?

Yes. Debit card chargebacks follow a similar process to credit cards and are governed by the card network (Visa or Mastercard). However, the protection window and exact rules may differ depending on your bank.

Q5. Is friendly fraud (chargeback fraud) illegal?

Filing a knowingly false chargeback can constitute fraud and, in some jurisdictions, is a criminal offence. While enforcement against individual consumers is rare, merchants can pursue civil action in certain high-value cases.

Q6. What is a chargeback reason code?

A reason code is a standardised numeric code assigned by the card network to categorise each chargeback. It determines what evidence the merchant needs to provide and the rules that govern the dispute.

Q7. What is the chargeback ratio?

The chargeback ratio is the number of chargebacks received in a month divided by the total transactions processed that month. Both Visa and Mastercard publish a 1% threshold — merchants who exceed it face monitoring programmes and potential penalties.

Q8. How do I avoid chargebacks as a merchant?

Use a clear billing descriptor, send order and delivery confirmations, implement 3D Secure authentication, maintain an accessible refund policy, and respond quickly to customer queries. Proactive communication is the single most effective prevention tool.

Q9. What happens if I ignore a chargeback notice?

If a merchant does not respond within the required window, the chargeback is automatically resolved in the customer’s favour. The merchant loses the disputed funds plus the chargeback fee, with no right to appeal that particular case.

Q10. Can I lose a chargeback even if the transaction was legitimate?

Yes. If a merchant fails to respond on time, submits incomplete evidence, or cannot meet the card network’s documentation requirements, the chargeback will be resolved in the cardholder’s favour even if the original transaction was entirely valid.

References & Resources

- 🔗 Visa Inc. — Visa Core Rules and Visa Product and Service Rules (official dispute & chargeback framework)

https://www.visa.com - 🔗 Mastercard International — Mastercard Transaction Processing Rules (chargeback lifecycle & reason codes)

https://www.mastercard.us - 🔗 PCI Security Standards Council — PCI DSS Documentation (merchant security guidelines)

https://www.pcisecuritystandards.org - 🔗 Reserve Bank of India — Guidelines on Regulation of Payment Aggregators and Payment Gateways

https://www.rbi.org.in - 🔗 National Payments Corporation of India — RuPay Network Rules and Dispute Management Framework

https://www.npci.org.in - 🔗 Consumer Financial Protection Bureau — Billing Disputes and Credit Card Protections

https://www.consumerfinance.gov - 🔗 Financial Conduct Authority — Section 75 and Chargeback Rights (UK)

https://www.fca.org.uk - 🔗 Electronic Transactions Association — Best Practices for Payment Dispute Management

https://www.electran.org

A chargeback is a forced reversal of a payment transaction initiated by a cardholder through their bank. It bypasses the merchant, returns funds to the customer, and is triggered by fraud, non-delivery, or billing errors.