A chargeback and a refund both return money to a customer — but they work very differently. A refund is issued voluntarily by a merchant, while a chargeback is a forced reversal initiated through the cardholder’s bank. Knowing which applies to your situation can save time, money, and unnecessary disputes.

Why This Distinction Matters More Than Most People Realize

Every day, consumers and businesses navigate payment disputes without fully understanding the tools available to them. Using the wrong mechanism — say, filing a chargeback when a simple refund would have resolved the issue — can damage merchant relationships, increase processing fees, and even lead to account termination for sellers. Read About – Merchant Management System

For merchants, chargebacks represent one of the most costly and disruptive financial challenges in modern commerce. For consumers, understanding the difference helps set realistic expectations about timelines, processes, and outcomes.

Key Takeaways: What You’ll Learn From This Guide

1. A refund is merchant-initiated and voluntary; a chargeback is bank-initiated and compulsory.

2. Always attempt a direct refund with the merchant before filing a chargeback.

3. Chargebacks carry fees, timelines, and account implications for merchants — and potential consequences for misuse by cardholders.

4. Friendly fraud is a significant and growing challenge for businesses of all sizes.

5. Consumer protection rights vary by country; understanding local regulations is important.

6. Payment processors play a central role in managing both refunds and disputes efficiently.

7. Clear merchant policies and good communication reduce the need for chargebacks significantly.

What Is a Refund?

A refund is a voluntary transaction in which a merchant returns funds to a customer. It follows the original payment path and is initiated from the seller’s side, typically through their payment processor or platform.

How Refunds Work

When a customer requests a refund, the process generally looks like this:

- The customer contacts the merchant directly.

- The merchant reviews the request and approves it.

- The merchant initiates a credit back through their payment system.

- The funds are returned to the original payment method, usually within 3–10 business days.

Common Reasons for Refunds

- Product returned in acceptable condition

- Service not delivered as described

- Duplicate charge made in error

- Order cancelled before fulfillment

- Customer dissatisfaction resolved at merchant level

Refunds are typically the fastest and least complicated resolution for both parties. When handled efficiently, they preserve customer trust and avoid escalation. Read about – Ecommerce Merchant Account Providers

What Is a Chargeback?

A chargeback is a forced reversal of a payment, initiated by the cardholder’s issuing bank — not by the merchant. It was originally designed as a consumer protection mechanism under regulations like the Fair Credit Billing Act (FCBA) in the United States.

How Chargebacks Work

The chargeback process involves multiple parties and is considerably more formal:

- The cardholder contacts their bank or card issuer to dispute a transaction.

- The bank investigates and provisionally credits the cardholder’s account.

- The merchant is notified and given a window to submit evidence (known as representment).

- The bank makes a final decision based on card network rules (Visa, Mastercard, etc.).

- Either the chargeback is upheld (merchant loses funds) or reversed (merchant retains payment).

Common Reasons for Chargebacks

- Unauthorized transaction – The cardholder didn’t make the purchase (fraud)

- Item not received – Product or service was never delivered

- Significantly not as described – Item differs materially from what was advertised

- Duplicate billing – Cardholder was charged more than once

- Credit not processed – Merchant agreed to refund but didn’t follow through

- Subscription cancelled but still charged – Recurring billing after cancellation

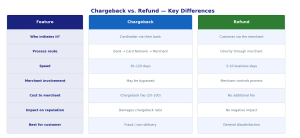

Chargeback vs Refund: Key Differences at a Glance

| Feature | Refund | Chargeback |

| Initiated by | Merchant | Cardholder (via bank) |

| Speed | 3–10 business days | 30–90 days or more |

| Cost to merchant | Minimal | Chargeback fee + potential penalty |

| Merchant involvement | Active resolution | Defensive response required |

| Impact on merchant account | None | Negative (affects dispute ratio) |

| Card network involvement | No | Yes |

| Consumer risk | Low | Low (but misuse can have consequences) |

| Best used when | Merchant agrees to return funds | Merchant is unresponsive or dispute is legitimate |

When Should a Customer Request a Refund?

A refund should always be the first step in resolving a payment issue. Contacting the merchant directly is faster, less bureaucratic, and often resolves the matter within days. Read About – Adult Site Merchant Account

You should request a refund when:

- The merchant has a clear return or cancellation policy that applies to your situation

- The issue is straightforward (wrong item, defective product, accidental order)

- The merchant is responsive and cooperative

- You are within the return window specified by the seller

Tip: Always keep records of your communication with the merchant. Emails, chat logs, and screenshots can be important if a dispute escalates later.

When Is a Chargeback Appropriate?

A chargeback is a last resort — a consumer protection tool to be used when the merchant is unwilling or unable to resolve a legitimate dispute.

Appropriate situations include:

- You were charged for a transaction you never authorized (genuine fraud or card theft)

- The merchant refused a valid refund request

- The product or service was never delivered and the merchant is unresponsive

- You received something materially different from what was described or advertised

- A promised refund was never actually processed

What Happens If You Misuse a Chargeback?

Filing a chargeback without genuine grounds is known as friendly fraud — and it has real consequences. Card issuers can flag accounts for misuse, and in serious cases, cardholders may lose dispute privileges or face collections on reversed funds. Read About – Best Adult Merchant Account Providers

Unlock Faster International Payment Approvals

Unlock smooth and secure international payments with our platform. Experience faster approvals, easy setup, and comprehensive support for global transactions. Take your business to new markets without delays or complicated processes.

Get Started NowThe Merchant’s Perspective: Why Chargebacks Are Costly

For businesses, a single chargeback is far more expensive than a refund. Here’s why:

- Chargeback fees typically range from $20 to $100 per dispute, depending on the payment processor

- Time investment is significant — gathering evidence, filing representment, responding to deadlines

- Dispute ratios are closely monitored by card networks; high ratios can result in merchant account suspension

- Reputational impact with payment processors affects future processing terms

According to card network guidelines published by Visa and Mastercard, merchants with dispute ratios above set thresholds (typically 1% of transactions) are placed in monitoring programs that carry additional fees and oversight. Read About – Machine Learning Payments

For this reason, many businesses invest in proactive customer service strategies — not just to keep customers happy, but to reduce chargeback exposure.

Friendly Fraud: The Growing Challenge for Merchants

One of the most significant issues in modern payments is the rise of friendly fraud — where a customer files a chargeback not because of genuine fraud, but to obtain a free product or service without returning it.

It’s estimated across the industry that a substantial portion of chargebacks represent cases where the cardholder did receive the product or service but still disputed the charge. This creates a real burden on merchants, particularly small businesses with fewer resources to manage disputes.

Best practices for merchants to combat friendly fraud include:

- Clear, prominent policies on returns, refunds, and subscriptions

- Delivery confirmation and order tracking on every shipment

- Signed agreements or receipts for high-value transactions

- Robust customer communication and support channels

- Billing descriptor names that customers will recognize on their statements

How Payment Processors Handle Both Scenarios

Payment processors like MyntPay facilitate both refunds and chargebacks, but in different ways.

For refunds, the processor routes the credit back through the original payment method quickly and with minimal overhead. Read About – Best PCI-Compliant Payment Gateways for Startups

For chargebacks, the processor acts as an intermediary between the card network, the issuing bank, and the merchant — managing deadlines, documentation requirements, and final fund settlements.

Merchants benefit from working with processors that provide clear dashboards for dispute management, timely notifications, and transparent fee structures. Understanding how your processor handles disputes before a problem arises is far better than discovering gaps when one occurs.

Chargeback Timeframes: What to Expect

Timeframes vary by card network and dispute reason code, but general guidelines are:

| Stage | Typical Duration |

| Cardholder dispute filing window | 60–120 days from transaction date |

| Bank provisional credit to cardholder | 1–5 business days |

| Merchant response window (representment) | 7–30 days (varies by network) |

| Final bank decision | 30–60 days after representment |

| Total resolution time | 45–90+ days |

These timelines can stretch further if arbitration is required — a process where the card network itself makes the final ruling.

Refund and Chargeback Rights by Region

Consumer protection rights vary depending on where a purchase takes place.

United States: The Fair Credit Billing Act (FCBA) and Electronic Fund Transfer Act (EFTA) provide federal-level protections for credit and debit card disputes.

European Union: The Payment Services Directive 2 (PSD2) governs dispute rights across EU member states, with strong consumer protections built in.

United Kingdom: Section 75 of the Consumer Credit Act provides additional protections for purchases made on credit cards between £100 and £30,000. Read About – Payment Gateway That Allows Adult Products

India: RBI guidelines on digital payment disputes and the Payment and Settlement Systems Act, 2007 govern dispute resolution frameworks.

Always review the regulatory framework applicable to your location, as rights, timelines, and processes differ meaningfully across jurisdictions.

Practical Checklist: Refund or Chargeback?

Use this decision guide to determine the right path:

Try a refund first if:

- ✅ The merchant is reachable and responsive

- ✅ You have a valid reason under their return policy

- ✅ The transaction was authorized by you

- ✅ You want a faster resolution

Consider a chargeback if:

- ✅ You did not authorize the transaction

- ✅ The merchant refused a legitimate refund request

- ✅ Goods or services were not delivered as promised

- ✅ A promised refund was never processed

- ✅ You have already attempted resolution with the merchant

Frequently Asked Questions

1. What is the main difference between a chargeback and a refund?

A refund is initiated voluntarily by the merchant and usually resolves within days. A chargeback is forced through the cardholder’s bank, takes weeks or months, and carries fees for the merchant.

2. Is a chargeback better than a refund?

Not necessarily. Refunds are faster and simpler. Chargebacks should only be used when a direct resolution with the merchant fails or when fraud is involved.

3. Can I get a chargeback and a refund for the same transaction?

No. If a merchant processes a refund and a chargeback is also filed for the same transaction, the cardholder may receive double the money. This is considered fraud and can have serious consequences. Read About – Ecommerce Merchant Processing

4. How long does a chargeback take to resolve?

Typically 45 to 90 days from the date the dispute is filed, though complex cases involving arbitration can take longer.

5. Does filing a chargeback hurt the merchant?

Yes. Beyond losing the disputed funds, merchants face chargeback fees, administrative time, and potential monitoring program placement if dispute ratios are too high.

6. What is friendly fraud in payments?

Friendly fraud occurs when a customer files a chargeback despite having legitimately received the product or service. It is a growing issue that costs businesses significant revenue annually.

7. Can a merchant dispute a chargeback?

Yes. Merchants can submit a representment — a formal response with evidence — to contest a chargeback. The bank or card network then makes a final decision.

8. How many days do I have to file a chargeback?

Most card networks allow cardholders 60 to 120 days from the transaction date or the expected delivery date to initiate a dispute, depending on the reason code.

9. What evidence should a merchant provide in a chargeback dispute?

Relevant evidence includes proof of delivery, signed receipts, communication records with the customer, clear refund policies, and transaction data matching the cardholder’s identity.

10. Are chargeback rights the same everywhere?

No. Consumer protection laws and dispute timelines vary significantly by country and card network. Always check the applicable regulations in your region.

A Note on Managing Disputes Proactively

Whether you’re a merchant managing high transaction volumes or a consumer navigating an unexpected billing issue, understanding the mechanics of refunds and chargebacks puts you in a stronger position.

For businesses, proactive dispute management — clear policies, responsive support, and transparent billing — reduces chargeback exposure before it becomes a problem. Platforms that offer real-time dispute visibility and structured workflows help teams respond faster and more effectively.

If you’re evaluating payment solutions for your business, look for partners who offer transparent chargeback management tools, clear fee disclosures, and dedicated support for dispute resolution. The right infrastructure can make a meaningful difference in how efficiently payment issues get resolved.

A chargeback is a forced payment reversal initiated by a cardholder’s bank, while a refund is a voluntary return of funds by the merchant. Refunds are faster and simpler. Chargebacks should only be used when direct resolution with the merchant fails.

References & Resources

- U.S. Federal Trade Commission (FTC) — Disputing Credit Card Charges: ftc.gov

- Consumer Financial Protection Bureau (CFPB) — Credit Card Dispute Rights and the Fair Credit Billing Act: consumerfinance.gov

- Visa — Dispute Resolution Rules and Operating Regulations: visa.com

- Mastercard — Chargeback Guide and Reason Codes: mastercard.com

- European Banking Authority (EBA) — Payment Services Directive 2 (PSD2) Guidelines: eba.europa.eu

- UK Financial Conduct Authority (FCA) — Consumer Credit Act Section 75 Guidance: fca.org.uk

- Reserve Bank of India (RBI) — Guidelines on Digital Payment Dispute Resolution: rbi.org.in

- Payment Card Industry Security Standards Council (PCI SSC) — Industry Best Practices: pcisecuritystandards.org

- Chargebacks911 Industry Research — Friendly Fraud and Dispute Trends: chargebacks911.com

- Merchant Risk Council (MRC) — Payments Risk and Fraud Resources: merchantriskcouncil.org