A dispute is a formal complaint a customer raises with their bank or card issuer about a transaction. A chargeback is what happens when that dispute escalates and the bank forcibly reverses the payment. Every chargeback begins as a dispute — but not every dispute becomes a chargeback. They are related, but they are not the same thing.

Why This Distinction Matters

If you are running an online business, processing payments, or managing customer transactions at any scale, you have almost certainly encountered the words “dispute” and “chargeback” used interchangeably. This loose usage is understandable in casual conversation, but it creates real confusion when things go wrong — and it can cost businesses money when they fail to respond appropriately.

Understanding exactly where one ends and the other begins is not a technicality. It directly affects how you respond, what documentation you need, and what your financial exposure actually is.

Key Takeaways: What You’ll Learn From This Guide

1. A dispute is any formal complaint a cardholder raises with their bank about a transaction. A chargeback is the escalated outcome — a bank-enforced reversal of funds.

2. Every chargeback begins as a dispute, but most disputes can be resolved before reaching the chargeback stage.

3. Chargebacks carry direct financial penalties for merchants, including non-refundable fees and potential account consequences.

4. Reason codes are the key to contesting a chargeback — merchants must respond specifically to the code issued, not just generically.

5. Friendly fraud — illegitimate chargebacks filed by customers who received what they paid for — is a growing problem across e-commerce verticals.

6. Prevention is far more cost-effective than contestation. Clear billing descriptors, fast customer service, and documented transactions reduce both disputes and chargebacks.

7. Businesses in higher-risk or digital-goods categories need processors and account structures built for their specific dispute environment.

What Is a Payment Dispute?

A dispute is the broader, more general term. It refers to any formal disagreement a cardholder raises about a transaction on their account.

When a customer sees a charge they do not recognize, did not authorize, or feel was fulfilled incorrectly, they can contact their bank and file a dispute. This initiates a formal review process governed by card network rules — primarily those set by Visa, Mastercard, and similar networks — as well as the policies of the issuing bank.

Common reasons a customer files a dispute:

- The item or service was not delivered

- The charge appears twice (duplicate billing)

- The amount charged does not match what was agreed

- The product received was significantly different from what was described

- The customer does not recognize the merchant name on their statement

- A fraudulent or unauthorized transaction appeared on the account

At the dispute stage, things are not yet final. There is still a window — often 30 to 45 days depending on the network and situation — for the merchant and customer to resolve the issue directly before it proceeds further.

What Is a Chargeback?

A chargeback is a specific mechanism within the dispute process. It is the bank’s unilateral reversal of a transaction — funds are pulled back from the merchant and returned to the cardholder.

Chargebacks were originally designed as a consumer protection tool. They give cardholders recourse when merchants are unresponsive, fraudulent, or simply unreachable. Card networks like Visa and Mastercard publish detailed rules about when chargebacks are permitted and what evidence merchants can submit in response.

Key characteristics of a chargeback:

- Initiated by the issuing bank (not the customer directly)

- Funds are removed from the merchant’s account immediately

- The merchant is typically charged an additional chargeback fee

- The merchant has the right to challenge it through a “representment”

- High chargeback rates can result in account termination by the payment processor

A chargeback is essentially the escalated, formalized outcome of an unresolved or unresolvable dispute. Once it reaches this stage, the process is governed by strict timelines and specific reason codes that determine how the case is evaluated.

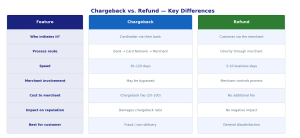

Chargeback vs Dispute: A Side-by-Side Comparison

| Feature | Dispute | Chargeback |

| Who initiates it | Customer contacts their bank | Bank acts on the customer’s behalf |

| Scope | Broad — covers any transaction complaint | Specific — a formal, enforceable reversal |

| Stage in process | First stage | Escalated stage |

| Funds status | Typically not yet reversed | Funds immediately reversed |

| Merchant involvement | May be contacted to resolve | Must respond with evidence or lose |

| Fees involved | Usually none at this stage | Chargeback fee charged to merchant |

| Resolution options | Direct resolution, refund, or escalation | Merchant wins or loses; arbitration possible |

| Timeframe | Days to weeks | Weeks to months |

How a Dispute Becomes a Chargeback

The transition from dispute to chargeback follows a defined sequence, though the exact steps vary by card network and bank.

1. Customer notices a problem The cardholder identifies a transaction they want to challenge — unauthorized use, delivery failure, or billing error.

2. Customer contacts their bank Rather than reaching out to the merchant first, the customer reports the issue to their card issuer. This formally opens a dispute.

3. Bank reviews and notifies the merchant The issuing bank evaluates whether the dispute has merit. In many cases, the acquiring bank — the merchant’s bank — is notified and passes the information to the merchant.

4. Merchant has an opportunity to respond This is the critical window. If the merchant provides compelling evidence (proof of delivery, refund confirmation, signed agreement), the dispute can be resolved without escalating.

5. Chargeback is issued if unresolved If the merchant does not respond, cannot counter the claim, or the bank determines the customer’s case is valid, a chargeback is issued. The reversal is processed automatically.

6. Merchant can contest through representment Even after a chargeback, the merchant may submit a representment — a formal challenge with supporting documentation. If successful, the funds are returned. If not, arbitration by the card network may follow.

Unlock Faster International Payment Approvals

Unlock smooth and secure international payments with our platform. Experience faster approvals, easy setup, and comprehensive support for global transactions. Take your business to new markets without delays or complicated processes.

Get Started NowFriendly Fraud: When Disputes Are Misused

A complicating factor in all of this is what the payments industry calls “friendly fraud.” This is when a cardholder files a dispute or triggers a chargeback not because of genuine fraud or a merchant error — but because they want to avoid paying for something they received and kept.

Examples include:

- A customer disputes a subscription charge after using the service for a month

- A buyer claims an item never arrived when tracking shows it was delivered

- A cardholder denies authorizing a purchase they made themselves

Friendly fraud is a significant challenge for ecommerce merchant account providers and payment processors globally. It accounts for a substantial portion of total chargeback volume, and it is increasingly difficult to distinguish from legitimate claims without strong transaction documentation.

How Disputes and Chargebacks Affect Merchants

For merchants — especially those in high-volume or higher-risk verticals — the financial and operational impact of disputes and chargebacks can be severe.

Direct financial costs:

- Lost revenue from reversed transactions

- Non-refundable chargeback fees (typically $20–$100 per case)

- Operational cost of gathering and submitting evidence

- Potential loss of merchandise if goods were already shipped

Indirect costs:

- Elevated dispute ratios trigger scrutiny from payment processors

- Exceeding card network thresholds can result in monitoring programs

- Repeated violations can lead to merchant account termination

The way ecommerce payment processing is structured, merchants are often at a disadvantage — they bear the burden of proof and face reversal-by-default unless they actively contest. This is why understanding the difference between a dispute and a chargeback early in the process is so operationally important.

The Role of Reason Codes

One of the most practical differences between a dispute and a chargeback is the introduction of reason codes at the chargeback stage. Card networks assign a specific reason code to every chargeback. These codes tell the merchant exactly what the cardholder claimed and what category of evidence is most relevant to contest it.

Visa reason codes (examples):

- 10.4 — Other Fraud: Card Absent Environment

- 13.1 — Merchandise or Services Not Received

- 12.5 — Incorrect Amount

Mastercard reason codes (examples):

- 4837 — No Cardholder Authorization

- 4853 — Cardholder Dispute

- 4863 — Cardholder Does Not Recognize Transaction

Understanding reason codes is essential for any merchant participating in a merchant management system or working with a high-volume acquiring relationship, because the entire representment strategy must be tailored to the specific code issued.

Unlock Faster International Payment Approvals

Unlock smooth and secure international payments with our platform. Experience faster approvals, easy setup, and comprehensive support for global transactions. Take your business to new markets without delays or complicated processes.

Get Started NowWhat Merchants Can Do to Reduce Both

Preventing disputes from reaching the chargeback stage — and reducing disputes overall — requires a combination of operational discipline and clear communication.

Before a transaction:

- Use clear, recognizable billing descriptor names (the name that appears on the customer’s statement)

- Provide transparent pricing, subscription terms, and cancellation policies

- Require cardholder verification for high-value transactions

At the point of transaction:

- Send immediate order confirmation with itemized details

- Capture proof of purchase, including IP address and device data for online orders

- For physical goods, use tracked shipping with signature confirmation where appropriate

After a transaction:

- Respond quickly to customer service inquiries — many disputes begin simply because a customer could not reach support

- Process legitimate refunds promptly; a refund is always cheaper than a chargeback

- Monitor dispute notifications and respond within the allotted window

Merchants using modern machine learning payment processing systems benefit from real-time fraud scoring and anomaly detection that can flag suspicious transactions before they even clear — reducing one of the most common chargeback triggers.

Industry-Specific Considerations

The dispute-to-chargeback dynamic plays out differently depending on the industry. In most retail and service verticals, clear documentation is sufficient to resolve the majority of disputes before they escalate.

However, certain industries face higher baseline dispute rates due to the nature of their products or delivery model. Subscription services, digital goods, and industries where the purchase is non-tangible tend to see elevated dispute volumes because there is no physical delivery to document.

Businesses operating in these categories — including those handling adult payment processing — are particularly exposed, since the digital nature of their products makes it harder to provide the kind of delivery evidence that quickly closes a chargeback case. These businesses often require specialized merchant accounts and processors familiar with their specific dispute landscape.

Frequently Asked Questions

Q1. What is the difference between a dispute and a chargeback?

A dispute is a formal complaint filed by a cardholder with their bank about a transaction. A chargeback is the specific outcome when the bank reverses the transaction in the customer’s favor. All chargebacks involve a dispute, but not all disputes result in chargebacks.

Q2. Who initiates a chargeback — the customer or the bank?

Technically, the bank (the card issuer) initiates the chargeback on behalf of the customer. The customer files the dispute; the bank decides whether to escalate it to a chargeback.

Q3. Can a merchant fight a chargeback?

Yes. Merchants can contest a chargeback through a process called representment, where they submit evidence that the transaction was valid. If the card network rules in their favor, the funds are returned.

Q4. How long does a chargeback process take?

Timelines vary by card network and complexity, but most chargeback cases resolve within 30 to 90 days. If arbitration is required, it can take longer.

Q5. What is a chargeback fee?

A chargeback fee is a penalty charged to the merchant by their payment processor each time a chargeback is filed, regardless of outcome. Fees typically range from $20 to $100 or more per case.

Q6. What is friendly fraud in the context of chargebacks?

Friendly fraud occurs when a cardholder files a dispute or triggers a chargeback despite having received and used the goods or services they purchased. It is a form of abuse of the consumer protection system.

Q7. Does filing a dispute automatically freeze the transaction?

Not always. Some banks place a hold on the disputed amount during review, while others allow the charge to remain while the investigation proceeds. Policies vary by issuer.

Q8. What is a chargeback reason code?

A reason code is a standardized identifier assigned by the card network to every chargeback. It tells the merchant what the customer claimed and guides what evidence should be submitted in response.

Q9. How many chargebacks can a merchant have before their account is at risk?

Card networks set thresholds — typically around 1% of transactions per month. Merchants who exceed these thresholds can be placed in monitoring programs and risk losing their merchant account.

Q10. Is it better to issue a refund or fight a chargeback?

In most cases, issuing a refund proactively is cheaper and faster. A refund avoids the chargeback fee and protects the merchant’s dispute ratio. Contesting should be reserved for cases of clear friendly fraud or documentation-backed wins.

A dispute is when a customer formally complains to their bank about a transaction. A chargeback is when the bank forcibly reverses the payment. Disputes can resolve without a chargeback, but every chargeback begins as a dispute.

References & Resources

Visa Core Rules and Visa Product and Service Rules — official dispute and chargeback procedures, reason codes, and merchant obligations. Available via Visa’s merchant support portal.

Mastercard Rules — published chargeback framework, timelines, and reason code documentation. Available via Mastercard’s merchant resource center.

PCI Security Standards Council (PCI SSC) — industry compliance framework for payment data security, relevant to dispute prevention.

Consumer Financial Protection Bureau (CFPB) — U.S. regulatory guidance on consumer dispute rights under the Fair Credit Billing Act.

Electronic Transactions Association (ETA) — industry best practice resources for merchant payment processing and risk management.

Chargebacks911 Industry Guides — educational resources on chargeback management, friendly fraud, and representment best practices.

Federal Trade Commission (FTC) — consumer guidance on disputing charges and understanding cardholder rights.